Commodities are surging and metals are loving their longest rally in seven years. Last year might have been a good one for metals, but this year will be even better.

For five straight quarters, six metals have risen, and this quarter's spike turns all our attention back to the miners: Gold is up 8.8 percent; silver is up 15 percent; aluminum and lead are both up 16 percent; and palladium is up 17 percent. But that's nothing compared to the run on lithium and cobalt.

Lithium continues is phenomenal rise, with the 'Big 5' producers--ALB, SQM, Tianqi, Ganfeng and FMC—in what lithium expert Joe Lowry calls a "can't lose" situation.

Lithium is up over 400 percent and there is a veritable stampede to get in on this commodity that is feeding our electric vehicle hunger.

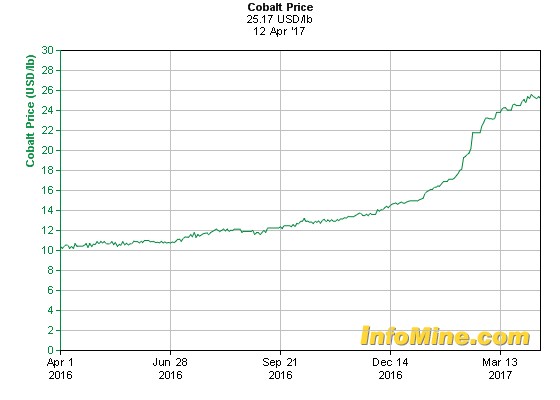

Cobalt stands to do even better, and because everyone's been paying attention to lithium in this rush, the real money to be made is here. There isn't enough, and what's available is unethically sourced from the Democratic Republic of Congo (DRC). Cobalt has made gains for 24 straight weeks, and the sky is the limit on this one.

Here are our top 5 mining picks right now:

#1 Katanga Mining (TSX:KAT)

This one might not be on your radar, but it should. In fact, few investors will have heard of it until recently, when it secured backing from Glencore for its projects in the Democratic Republic of Congo, where it is sitting on very large, high-grade reserves of copper and cobalt.

Katanga has a 75 percent interest in the Kamoto copper-cobalt mine; and while weak copper prices halted production in the mine in 2015, it is expected to re-open (with cost-saving modernizations) in 2018 and ramp up production significantly. But sweetening this deal is the fact that Glencore (the largest producer of cobalt in the world and a major player in DRC) is backing KAT with a massive loan that will make this all feasible. We see good times ahead for Katanga.

#2 Scientific Metals (TSX:STM.V; OTC:SCTFF)

As hedge funds start hoarding cobalt ahead of the demand surge and suppliers start panicking, Scientific Metals has stepped in with a major new acquisition in the most (ONLY) prolific cobalt mining belt in the U.S.

Welcome to the Idaho Cobalt Belt, where Scientific Metals in late February acquired Iron Creek Cobalt, one of only two cobalt mines slated to come into production in the next few years (the other is located in the same belt).

In this acquisition, the company scooped up property that has already seen a substantial amount of historical exploratory work that includes 30,000 feet of diamond drilling. Iron Creek has a historic resource of 1.3 tons of cobalt with blue sky potential of up to 10 million tons.

This small-cap looks even better when you consider its management. CEO Wayne Tisdale and his team at Intrepid Financial have in recent years created $2.7 billion in value by building and selling 5 companies in completely different industries—and one of them was a homerun hit in lithium. We like the odds here because cobalt is already a clear winner: prices are climbing, supply is already short, and demand is set to surge explosively, while Scientific Metals is pretty much assured of a seat at this feast-worthy table.

#3 Agnico Eagle Mines (TSX:AEM)

For gold, we're looking at Agnico to benefit nicely from rising gold prices now because it's been beaten down until recently, when it finally showed up with solid Q1 earnings, with revenues in at nearly $500 million.

The Canadian gold producer also beats analysts' expectations on first-quarter revenue by $35.7 million. So while these stocks have taken a hit in the recent past, AEM is back on investor radar and is outperforming—with room for shares to keep growing for now.

About this time last year, a majority of analysts were telling us to buy Agnico. Then there was a period that was clearly a sell. But now we're moving back into 'buy', and nearly half of analysts would agree. It's again gaining in popularity.

One catalyst will be the results of a January deal to acquire a 19.9 percent interest in White Gold Corp. And there is a lot of near-term project potential here, with a very nice pipeline.

- AEM's La Ronde Complex in Quebec could be adding more production soon;

- We're looking at solid development prospects and advancements at AEM's Goldex project in Quebec;

- New production could also come from the Canadian Malartic project;

- There is the potential to expand to 2.0 million tonnes per year at the Kittila (Finland) mine;

- And everyone's eyeing some exciting exploration prospects at the company's property in Mexico.

#4 Franco-Nevada Corporation (TSX:FNV)

This CAD $15.52-billion market cap company ties returns to the price of gold without risky exposure to direct ownership and operatorship of mines.

FNV ended 2016 with a relative bang. But this is a unique case because it doesn't own or operate any mines—so this is for the investor looking for a different kind of exposure to the metals rally: FNV secures precious-metal streams.

So, the company's growth last year was thanks to the new streams it acquired, including the prolific South Arturo mine in Nevada (operated by Barrick and Premier Gold Mines), Glencore's Antapaccay mine in Peru, and Teck Resources (see below—it's another of our top 5 picks) Antamina mine, also in Peru.

Franco-Nevada has a brilliant cash flow. This is likely attributed to its bigger exposure to gold. Gold, after all, accounted for 70 percent of its total 2016 revenues. It also has a more diversified portfolio than its peers. And growth prospects also look good—particularly in oil. On track is a Midland Permian Basin stream of around $110 million in oil and gas royalty rights and another similar value stream in Oklahoma's STACK play.

Overall, the next few years should be very kind to FNV.

#5 Teck Resources Ltd. (TSX:TECK-B)

If it's sheer diversification that comforts you, Teck Resources is a great bet. All three of its core target metals (metallurgical coal, copper and zinc) have seen price rebounds.

Last year saw a solid coal rally thanks to Chinese moves to limit the number of days mines can operate in a year. This took a lot of pressure off supply, and prices responded nicely. In fact, it went from oversupply to tight supply, pushing coal prices from $90 to over $300 in November, which later dropped to about half when China stepped in to ease its restrictions in an attempt to rebalance the market. But Teck had already benefitted nicely, as shown in its Q4 results. Teck sells most of its coal on quarterly contracts, and was expecting even better results in Q1 2017.

Teck also benefitted from a big run for zinc last year.

But what we really like is its further diversification: Now it's getting into oil sands and it's shown financial and managerial savvy in its efforts to meet the development costs of its Fort Hills Oil Sands project, which expects its first oil by the end of this year. This is important because this play has a 50-year reserve life. It's a pretty good time to get in on Teck, before this oil starts flowing.

Honorable Mentions…

- Lithium America's Corporation (TSX:LAC): Lithium is all the rage (even if it's about to be trounced by cobalt), and this small-cap miner has an enviably low debt load.

- Taseko Mines (TSX:TKO): Operations are improving, and production costs are dropping, bumping Taseko's shares up, and clearing a path for a better year, while share prices are still low enough to be an attractive bet.

- Cameco Corporation (TSX:CCO) (NYSE:CCJ): Cameco—a U.S. $4.52-billion market cap company--is trading at a major discount to its intrinsic value right now, and it's a good play for dividend-focused investors.

- Fortuna Silver Mines Inc. (TSX:FVI): Catalysts included work on a feasibility study prepared in 2016 in Fortuna's 100 percent owned Lindero gold project in Argentina's Salta Province.

Legal Disclaimer/Disclosure: This piece is an advertorial and has been paid for. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this Report should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. We make no guarantee, representation or warranty and accept no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Baystreet.ca only and are subject to change without notice. Baystreet.ca assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.