PREFACE

We find a very powerful outcome examining short put spreads for Oracle Corporation when we use a clever earnings risk management approach. This is the information that the top 0.1% have and now it's time for us all to see it.

With relative ease we can become experts -- to see the risks we want to take and see those that we want to avoid, which ultimately allows us to optimize our results. This is one of those cases.

STORY

There is a lot less 'luck' involved in successful option trading than many people have come to understand. We can get specific with short put spreads on ORCL in this dossier. Let's look at a three-year back-test of a short put spread strategy and use the following easy rules:

* Test monthly options, which means rolling the put spread every 30-days.

* Avoid holding a position during earnings.

* Study an out of the money put spread -- specifically the 30 delta / 10 delta spread.

* Test the put spread looking back at three-years of history.

More than all the numbers, we simply want to walk down a path that demonstrates that it is actually quite easy to optimize our trades with the right tools. In the set up image below we just tap the rules we want to test.

Next we glance at the returns.

RETURNS

If we did this 30 delta / 10 delta short put spread in Oracle Corporation (NYSE:ORCL) over the last three-years but always skipped earnings we get these results:

| Sell 30 Delta Put, Buy 10 Delta Put |

| * Trade Frequency: 30 Days |

| * Back-test length: three-years |

| * Always Avoid Earnings |

|

| Gross Gain: |

$1,014 |

| Gross Loss: |

-$854 |

| Short Put Spread Return: |

30.7% |

| Stock Return: |

6.2% |

|

| Option Out-performance |

24.5% |

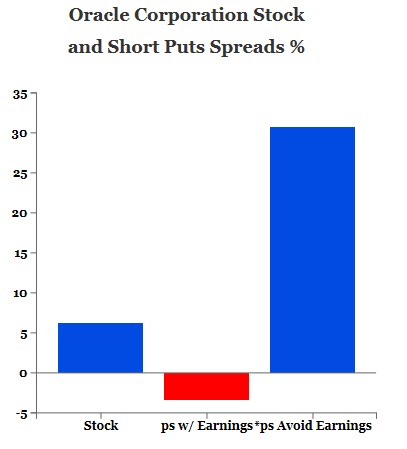

First we note that the short put spread strategy actually produced a higher return than the stock 30.7% versus 6.2% or a 24.5% out-performance.

Selling a put spread spread every 30-days in ORCL has been a pretty substantial winner over the last three-years returning 30.7%. Even better, the strategy has outperformed the short put spread that was held during earnings. Let's turn to that piece, now.

OPERATING FURTHER WITH ORACLE CORPORATION

That initial move -- examining short put spreads while avoiding earnings is clever. It definitely gets us a study ahead of most casual option traders. But we can move our knowledge yet further.

The next move will implement the same back-test rules and deltas, but this time we will only test results during earnings. To be perfectly clear, we test the short put spread that is opened two-days before earnings, lets earnings occur, and then closes the option position two-days after earnings.

Here are those results for the same 30 delta / 10 delta short put spread:

| Sell 30 Delta Put, Buy 10 Delta Put |

| * Trade Frequency: 30 Days |

| * Back-test length: three-years |

| * Only Trade Earnings |

|

| Gross Gain: |

$286 |

| Gross Loss: |

-$302 |

| Short Put Spread Return: |

-3.4% |

Selling a put spread in Oracle Corporation during was not only a loser, more importantly, it returned less than the same short put spread that avoided earnings. While this clever use of avoiding earnings has outperformed the short put spread that was held during earnings, there's a bigger picture here. Let's turn to that piece, now.

CLARITY

For clarity we chart the stock returns, the short put spread (ps) strategy with earnings and the one that avoids earnings, below.

TRADING TRUTHS

This approach on Oracle Corporation (NYSE:ORCL) goes way further than returns. What we have done is seen rather explicitly that the concept of expertise in options has been made overly complex. The concept here is straight forward: securing knowledge before entering an option position constructs a mind set about what to trade, when to trade it and even if the trade is worth it at all. Now we can see this practice taken further, beyond Oracle Corporation and put spreads.

WHY THIS MATTERS

When we wrote that there's actually a lot less 'luck' and a lot more planning in successful option trading than many people know, this is what we meant.

It's not about trying to guess which stocks will go up or down.

What the back-tester allows us to do is find calm, low stress stocks or ETFs (like SPY, QQQ, etc), and in this case, ORCL, and find the option strategies that have created a high percentage of winning trades, gaining profitability slowly, while avoiding unnecessary risks - specifically, avoiding earnings.

In a five minute video, your entire view of the options world and what people mean when they say 'expert trader' will be turned upside down - to your advantage.

Tap here to see the CML Pro option back-tester.

Thanks for reading, friends.

Risk Disclosure

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.